Are readers still buying books new? How important is affordability when choosing a book? And what does this mean for publishers trying to navigate an economically cautious consumer landscape? We answer these questions using insights from SalesData, the Canadian Book Consumer Study 2024, The Canadian Book Market 2024, and the Canadian Leisure & Reading Study 2024.

Where are people buying books?

According to the Canadian Book Consumer Study 2024, 48% of respondents reported buying new books in both 2023 and 2024, while 21% in 2023 and 20% in 2024 said they bought used.

When deciding where to buy, the financial motivators for purchasers in 2024 were:

Good price at 29%

Cheap or free delivery at 19%

Loyalty card availability at 11%

These findings suggest that while convenience and loyalty incentives matter, price remains a priority when it comes to retail choice.

Keeping this in mind, retailers may benefit from enhancing strategies that reduce barriers to purchase and increase customer retention:

Strengthening or introducing loyalty programs may encourage repeat buying behaviour as shoppers seek greater value.

Prioritizing deals and promotions may be used as a hook to get potential book buyers into a brick-and-mortar or virtual bookstore.

Promoting affordable or free delivery options across all channels can help drive conversions and support overall sales growth as delivery costs influence buying decisions.

We were also curious about whether the GST/HST relief for physical books had any impact people’s buying decisions, however with only 2% of respondents selecting that option for the applicable timeframe in 2024, it doesn't appear that was a major influence on consumer book spending.

What are people spending?

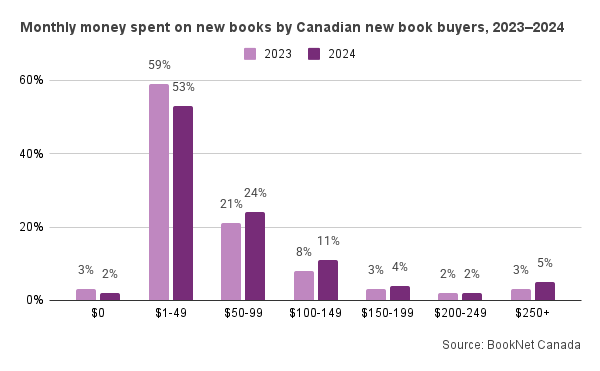

Looking at overall book spending, the Canadian Leisure & Reading Study 2024 shows that most readers spend between $1 and $49 per month on books regardless of whether they were buying print books, ebooks, or audiobooks. This was true in both 2023 and 2024.

When asked how they obtain books:

46% in 2024 (44% in 2023) said they choose books that fit their budget

31% in 2024 (33% in 2023) reported borrowing or getting free books

23% in both years reported no financial limitations

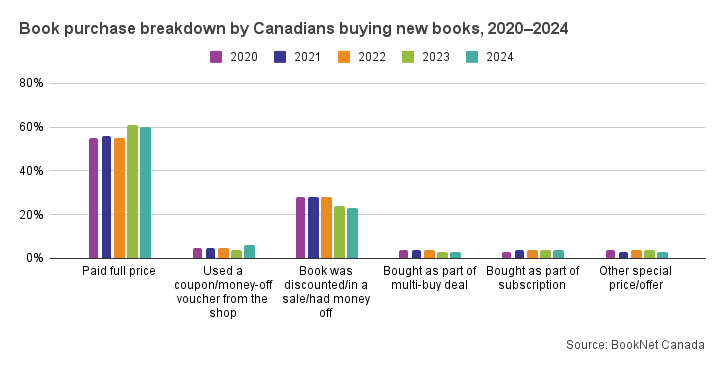

In terms of actual transaction price, in our surveying for the Canadian Book Consumer Study 2024 we found that the majority of purchases were made at full price (60% in 2024 and 61% in 2023). Discounted or on-sale books made up 23% of purchases in 2024 and 24% of purchases in 2023, while the use of coupons, subscriptions, or multi-deal purchases each remained under 7%.

Still, even with most purchases being full-price, 85% of readers surveyed for the Canadian Book Consumer Study 2024 felt they received good value for the money they spent on books. Similar value sentiment (over 80%) was reflected across all formats in the Canadian Leisure & Reading Study 2024.

Affordability by format

Affordability plays a particularly strong role in influencing format choice. According to the Canadian Leisure & Reading Study 2024, when deciding to purchase a book 48% of print readers in 2024 (46% in 2023), 39% of ebook readers in 2024 (37% in 2023), and 32% of audiobook listeners in 2024 (34% in 2023) said affordability was important.

There was also a near-even split among readers who reported buying within their budget vs. those who had unlimited spending flexibility, as found in the Canadian Book Consumer Study 2024, underscoring the need for publishers to cater to both budget-conscious and financially flexible buyers.

Comparing prices and seeking deals

Even though most book buyers reported paying full price, many are still strategic. In the Canadian Book Consumer Study 2024, 16% of respondents in 2024 (18% in 2023) said they compared prices across multiple retailers before making a purchase.

To act on this insight, retailers should ensure their pricing remains competitive or, if higher, they should clearly highlight the added value (such as premium design, bundled content, or limited editions) to justify the cost and attract value-conscious consumers.

How Prices Have Changed

According to The Canadian Book Market 2024, median list prices increased across most formats and genres between 2020 and 2024. The largest price gains were seen in Juvenile, Young Adult, Fiction trade paper formats, as well as Non-Fiction hardcovers.

There were two notable exceptions, YA titles and Non-Fiction mass market books remained stable in price over the same period.

Percent Increase of Median List Prices by Format from 2020 to 2024

Fiction

All Formats - 15.29%

Mass Market - 0.00%

Trade Paper - 9.48%

Hardcover Trade - 5.71%

Non-Fiction

All Formats - 14.00%

Mass Market - 4.25%

Trade Paper - 8.89%

Hardcover Trade - 14.26%

YA

All Formats - 23.60%

Mass Market - 0.00%

Trade Paper - 20.01%

Hardcover Trade - 6.08%

Juvenile

All Formats - 27.41%

Mass Market - 11.12%

Trade Paper - 25.13%

Hardcover Trade - 9.10%

Even amidst rising prices, 85% of readers said they felt they received good value for the money they spent on books in 2024, according to both the Canadian Book Consumer Study 2024 and the Canadian Leisure & Reading Study 2024.

One value add that’s worth highlighting is the rise of special edition publishing, particularly in the Fantasy and Romance categories, which continue to see explosive growth. As shared during our On the rise: Book subjects on the move in the Canadian market session at Tech Forum, Fantasy / Romance sales rose by 82%, Romance / Fantasy by 175%, and Young Adult Fiction / Fantasy / Romance by 101%, with demand showing no signs of slowing down. While collector’s editions have long been available for literary classics, today’s deluxe editions are being marketed as enhanced, value-added experiences, and it seems readers agree.

How does the consumer price index affect book prices?

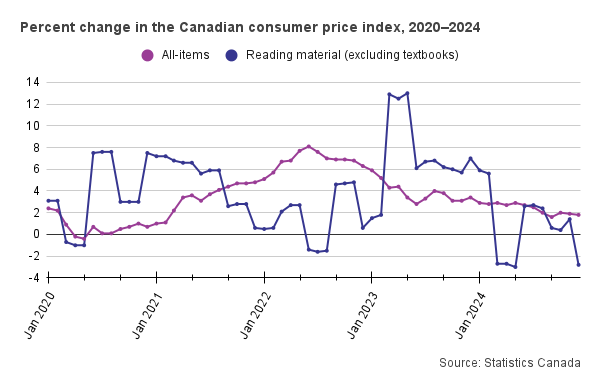

When discussing book affordability and value, it’s useful to situate those trends within a broader economic context. The consumer price index (CPI) measures the average change in prices paid by consumers over time.

From 2020 to 2024, the changes in Canada’s “all-items CPI” reflected the broader cost-of-living changes across goods and services. During that same period, prices for “reading material” followed their own trajectory, one that at times diverged significantly from overall inflation.

In mid-2022, when general inflation hit a high, the CPI for reading material actually declined, indicating that book prices were not increasing at the same rate as most consumer goods.

By early 2023, that trend reversed, with book prices rising dramatically (up 13% in May 2023) outpacing inflation in most other sectors.

In 2024, the pattern flipped again. The CPI for reading material dropped significantly mid-year and ended 2024 with a -2.8% fall, even as the overall inflation rate increased by 1.8%.

These trends suggest that while books are not immune to inflationary pressures, the pricing of reading material is influenced by more than just economic inflation.

Strategies for retailers and publishers

Canadians continue to show a strong interest in reading — but they’re doing so with a keen eye on their wallets.

As consumer caution grows, retailers can:

Create dedicated displays for value-oriented titles

Highlight books that offer clear bang for the buck whether they’re deluxe editions, part of a multi-book bundle, or currently on sale.Make it easy to find books by budget

Organize in-store or online sections like “Books Under $20,” or “Best Value Reads.”Promote loyalty programs and free shipping thresholds

Since 29% of readers chose a retailer due to good pricing and 19% cited free or cheap delivery (Canadian Book Consumer Study 2024), communicate these perks clearly.Reinforcing perceived value

Highlight aspects like premium design, bundled content, or limited editions to justify full-price purchases. CataList users can login to their account to see marketing info and key selling points entered by publishers to aid with this endeavour.

Publishers can:

Highlight value-adds in metadata and catalogues

Communicate key selling features like deluxe packaging, foil stamping, sprayed edges, bonus content, or bundled digital materials directly in your title metadata and seasonal catalogues. Make it easy for retailers and readers to understand the value.Support subscription and bundling models

Explore partnerships or formats that allow for bundle deals, digital and print combinations, or series sets.Encourage discovery through borrowing

With many readers relying on libraries or borrowing networks, ensuring titles are accessible through non-retail channels can boost exposure and long-term engagement.Provide flexible ordering options

Some retailers may prefers to prioritize more affordable titles while carrying only a select number of premium editions, in accommodating these kinds of strategies and working alongside retailers, this can serve as a way to inspire creative initiatives to support your titles more effectively.

Even with rising list prices and tighter budgets, Canadians continue to believe books are worth the money. By understanding where, why, and how readers are making purchase decisions, publishers can tailor their pricing, format offerings, and marketing strategies to meet readers where they are without compromising long-term value.

This blog post outlines strategies for streamlining ONIX creation, maintenance, and distribution.